Making a budget might seem overwhelming at first, but hear this: You can do it. How? By breaking down the process a bit. Because no one eats an elephant by swallowing it whole. (You go one bite at a time.) And no one leaps into budgeting like a pro. (You take it one step at a time.)

So, here we go—bite by bite, step by step. Here’s how to make a budget in five steps.

- List Your Income

- List Your Expenses

- Subtract Expenses from Income

- Track Your Transactions

- Make a New Budget Before the Month Begins

What Is a Budget?

Real quick though, let’s define the word budget. A budget is just a plan. It’s not a restriction on spending—it’s a plan for what you’ll do with your money. It’s a plan for what’s coming in and what’s going out.

When you learn how to make a budget—and do it every month—you’re giving your money purpose. You’re taking control. Goodbye, money anxiety. Hello, money goals.

Keep reading to see how to make it happen so you can make a budget that works for you.

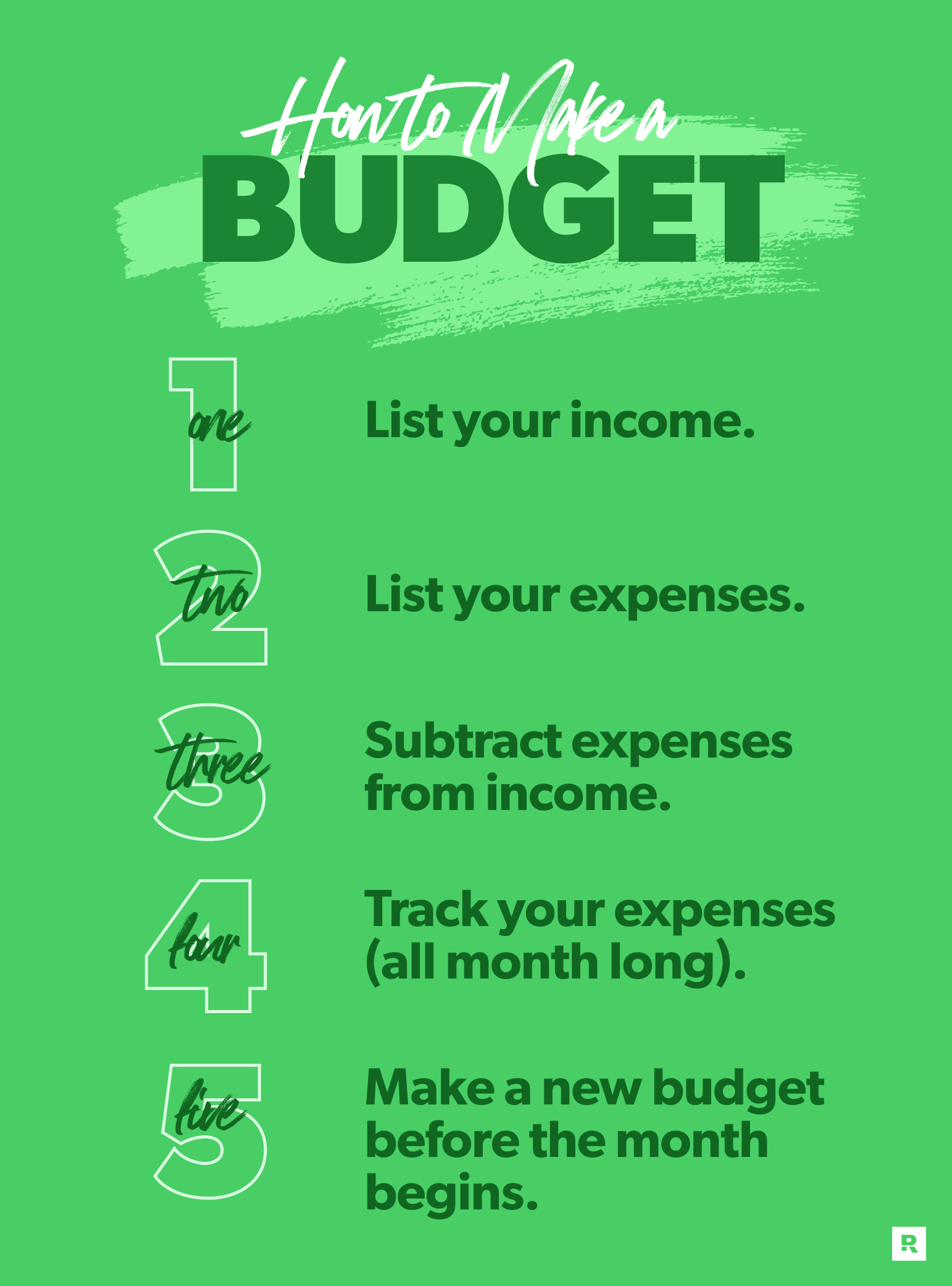

How to Make a Budget in 5 Steps

No matter how you feel about budgeting right now, no matter what money goals you have, and no matter your income—you can make (and keep!) a budget in just five steps.

First, decide if you’re making a budget on paper, with a spreadsheet or in an app. (We know a great tool called EveryDollar. Just saying.) Either way, it’s totally okay to start by writing out everything on a sheet of paper.

Pro Tip: Before you dive into the steps, open up your online bank account or grab your bank statements. That will give you the info you need as you start filling out numbers on your budget.

Step 1: List Your Income

Income is any money you plan to get during that month—that means your normal paychecks and any extra money coming your way through a side hustle, garage sale, freelance work or anything like that.

You work weekends as a barista or bagpiper for hire? That’s income and it goes in your budget.

Create separate income budget lines for every paycheck you (and your spouse) make, plus anything extra coming in. Note: You’re working with net income here, meaning what you bring in after taxes or anything else that’s taken out of your paycheck. Here’s an example:

His Paycheck 1: $1,500

Her Paycheck 1: $1,500

His Paycheck 2: $1,500

Her Paycheck 2: $1,500

Side Hustle: $500

Total Income: $6,500

If you’ve got an irregular income, take a look at what you’ve made the last few months and list the lowest amount as this month’s planned income budget line. You can adjust later in the month if you make more and add that extra money to your money goal or another budget line.

Step 2: List Your Expenses

Now that you’ve planned for the money coming in, you can plan for the money going out. It’s time to list your expenses! (Yep, this is when that bank account or statement gets super helpful.)

Pro Tip: When you’re making a budget, before you put in all the things you’ll pay for this month, set aside money for giving. We believe in 10% of your income here and always having a spirit of generosity! Next, budget for your savings goals, like an emergency fund (depending on your Baby Step, which we'll talk about more in a minute). You've got to pay yourself first before you pay everyone else!

What’s next?

Cover your Four Walls. That’s food, utilities, shelter and transportation. Make a budget category for each of these and create budget lines underneath for your specific expenses.

Start budgeting with EveryDollar today!

Think of a budget category as a folder, and the lines as the files inside it. Or the category is like a playlist, and the lines are like the songs. Or . . . okay, you get it.

Here’s what it might look like for you (but with your numbers, of course!):

Budget Category: Food

Groceries: $400

Budget Category: Utilities

Electricity: $75

Water: $50

Natural Gas: $20

Budget Category: Shelter/Housing

Mortgage: $1,500

HOA fees: $50

Budget Category: Transportation

Gasoline: $200

Some of these are called fixed expenses—aka the expenses that stay the same every month, like your rent or mortgage.

Other expenses change up, like groceries or gasoline. By the way, that grocery budget line is super hard to guess at first, so just start with a really good estimate based on your past spending. You’ll learn better what you actually need here in the months ahead.

Next, list all other monthly expenses. Start with the essentials: We’re talking about insurance, debt, childcare, etc. Then work in a miscellaneous line and any nonessentials like personal spending, fun money and entertainment.

Then use your online bank account or those bank statements to estimate what you plan to spend for everything.

Here’s a quick callout. If you’re working to save money, get out of debt, or some other money goal, you’ll get there way quicker if you cut back on the nonessential spending.

If you don’t know what goal to focus on right now, check out the 7 Baby Steps. This plan breaks the most important money goals into easy-to-understand, actionable steps!

Make new budget categories for your new budget lines. Of course, if you spend money eating out, you can just add a line called Restaurants under your Food category—as long as you remember groceries are a necessity, but drive-thrus or fancy three-course meals out are not.

Step 3: Subtract Expenses From Income

Math time! (It won’t be too bad. But it is totally necessary. Let’s do this.)

Subtract all your expenses from your income. This number should equal zero. We call this a zero-based budget.

This is key: A zero-based budget doesn’t mean you let your bank account reach zero. Leave a little buffer in there of about $100–300.

It also doesn’t mean you blow all your money. And here’s the reason we love this method. Zero-based budgeting just means you give every dollar a job to do: spending, giving, saving or paying off debt. It’s all accounted for and given a purpose.

You work hard for your money, right? Well, it should work hard for you! Every. Single. Dollar.

Okay, though, what do you do if you subtract your expenses from your income—and you’ve got money left over? Don’t leave it there. You’ll end up mindlessly spending it on coffees, convenience store candy, and those one-click deals of the day. Get those dollars to work by putting any “extra” money toward your current money goal.

What if you end up with a negative number? Eck, right? It’ll be okay. You just need to cut expenses until your income minus your expenses equals zero. (Hint: Start with those eating out and entertainment budget lines. If restaurants are your love language, this will hit hard. But you can’t spend more than you make. You got this!)

If you’re still struggling to make ends meet, don’t forget the power of the side hustle or overtime. Just remember not to increase your spending when you increase your income. Your extra cash needs to cover your budgeted expenses.

Is the math stressing you out a little? Listen, let EveryDollar do that for you. Our free budgeting app is made for this zero-based budgeting stuff, and you won’t have to keep running back to the calculator to get it right.

Okay, so that’s it for making a budget. The next two steps are all about sticking with it.

Step 4: Track Your Expenses (All Month Long)

Ready for one of the biggest secrets for how to budget—and do it really, really well? Good, because we don’t want to keep it a secret. Here it is: Track. Your. Transactions.

Every single one.

Putting the plan on paper, in your spreadsheet, or in your app is just a bunch of good intentions without this step. It’s like writing down a goal to run a marathon, making a training plan, lacing up your shoes, and flopping on the couch with a bag of donuts.

What are we talking about? Tracking your transactions means you account for everything that happens with your money all month long.

When you fill up the gas tank, subtract that expense from transportation. When you pay the rent, subtract that expense from housing. When you buy a coffee on the way to the office, subtract that expense from your personal spending (or whatever budget line you made for the perk that helps you work).

Track your transactions regularly. That might be at the end of each day, or it might mean you log in a purchase before you leave the grocery store parking lot. Or it might mean once a week. Whatever works for you and gets every expense tracked.

As you’re tracking, make adjustments as you need to. Yes, really! This is your budget. You make it work for you. If the electricity bill comes in higher than you thought, just tweak another budget line to make up for it. If the water bill comes in lower, then celebrate and move that money over to your current money goal—or add it to a budget line that went over.

We can’t say enough good things about tracking your transactions. But to sum up, we love this budgeting step because it’s how you:

- Stay accountable to your budget, yourself and your money goals. (Also your spouse, if you’re married! And remember EveryDollar? You two share an account, so you’re budgeting as a team!) No secrets. No pretending a purchase didn’t happen.

- Keep from overspending, because as you enter expenses, you see what you have left in every budget line! Instantly you’ll know what’s left so you don’t overspend.

- Stay on top of the budget. Your budget is not a set-it-and-forget-it project. It’s not a slow cooker. When you track transactions, you get in your budget all the time, and you can make adjustments so you know where your money is going—all the time.

- Learn and adjust your spending habits so you can get back on track with your goals and finally make them happen. One monthly budget at a time.

Step 5: Make a New Budget Before the Month Begins

While your budget shouldn’t change too much from month to month, the fact is, no two months are exactly the same. That’s why you create a new budget every single month—before the month begins. Then you can stare down certain expenses and say, “You will not be a surprise to my bank account, thank you very much.”

When you’re ready to start your next budget, just copy over this month’s budget to the next, and then make changes for anything new that’s coming.

Here are some examples of month-specific expenses to prep for:

- Celebrations like birthdays and anniversaries: Never forget those.

- Holidays: Do you need decor, gifts or a feast at the ready?

- Seasonal purchases: Don’t forget to budget for back-to-school season, fall coffee flavor releases, and your spring kickball league.

- Semiannual expenses: Do you pay your auto insurance twice a year? Do you need an oil change next month?

- Annual expenses: Is it time for your yearly eye exam? Do you need to budget for your pet because Sir Barksalot needs to get his shots at the vet?

Here’s one way to handle getting these changing expenses into your budget:

- Create a budget category called something like Month-Specific Stuff or Alternating Expenses or Discretionary (if you like huge words).

- Then add whatever lines you need for that month and delete the ones from last month you no longer need.

Where does the money come from? You can cut back spending somewhere else and move that money over to this category. Taking $5–20 from a couple budget lines really adds up. Literally. Or if you can, crank up your income for the month. (Time for an extra freelance gig!)

Hey, if this part sounds complicated or clunky, that’s because it can be at the beginning. It takes people about three months to really get the hang of budgeting, so give yourself some grace and keep working on it! The benefits of budgeting will far outweigh the effort.

Why Making a Budget Is So Important

What are the benefits? Why is it worth it? Because budgeting tells your money where to go—instead of you wondering where it went. It shows your money who’s in charge. (You.)

Budgeting is how you make any money goals happen—it’s how you make progress with your finances! It puts you in control. It gives you permission to spend your money your way.

We could go on and on and on because we honestly believe making a budget—and living that budgeting life—is one of the most important decisions you’ll make with your finances.

How to Make a Budget With Confidence

That’s it! That’s how to make a budget—and why you should. So, now it’s time to do it! It’s time to get confident with your money.

But what about being confident with budgeting? Hey—let EveryDollar help! This free tool makes budgeting easier, which helps you win with money!

And guess what? When you get the premium version of EveryDollar, well—it’s even easier.

You’ll get features like budget reports, which show you trends in your income and spending. Then you can see if those spending habits line up with your money goals.

You’ll also get our personal favorite: bank connectivity. You won’t have to type in every single transaction. They’ll stream right on in. You just drag and drop them to the right budget line.

So, check out those premium EveryDollar features! You can budget with confidence—every single month.

Get that premium version of EveryDollar today!

Did you find this article helpful? Share it!

About the author

Ramsey Solutions