Owning a small business has its perks, right? You get to be your own boss, set your own hours, make your own decisions. But no matter how much fun you have running the show, there’s one thing about owning a small business that makes most small-business owners cringe.

Yep, you guessed it—calculating small-business taxes.

It’s not everyone’s favorite weekend activity, but unfortunately, you have to calculate your small-business taxes at least once a quarter. There’s a lot that goes into this, so put your nerd hat on and let’s dive right in.

How Is Your Business Legally Structured?

First off, before you touch a single spreadsheet, make sure you’re clear on the legal structure of your business. Whether you run a bookstore or a research consulting firm, the IRS will classify your business as one of the following five structures: sole proprietorship, partnership, LLC, S corporation, or C corporation.

The IRS will classify your business as one of the following five structures: sole proprietorship, partnership, LLC, S corporation, or C corporation.

For the head scratchers out there, thinking, Well, I don’t know—I just own a small business, the IRS is probably classifying you as a sole proprietorship. If that doesn’t sound right to you, take a second and get a refresh on each of the business structures.

How Do You Calculate Income Taxes for Small Businesses?

Do you remember how you calculated income taxes for your personal filing? You took your yearly income and subtracted deductions and credits to get your taxable income. That taxable income put you in certain tax brackets, with each bracket corresponding to a tax rate. Finally, you multiplied your tax rate and your taxable income to get how much you owed the IRS. Easy, right?

Calculating small-business taxes isn’t much different, especially if your business is a sole proprietorship, partnership, LLC, or S corporation (we’ll come back to these in a minute). C corporations are a little bit different, so it’s worth spending a few words on them.

What’s the tax rate for C corporations?

C corporations are taxed twice, once at a corporate rate of 21% and then again at their shareholders’ personal rates (if they take a dividend).1

For example, let’s say you own a company called Money Makeover Inc. Suppose your company brought in $200,000 in profit. And let’s also go ahead and say that after business expenses and deductions, you’re left with $175,000 of taxable income.

So, first, Money Makeover Inc. has to pay taxes at the corporate level, which is a flat rate of 21%. Remember: No matter how much profit Money Makeover Inc. makes, it will always pay a flat 21% for income taxes. In our example, that would be:

$175,000 x 21% = $36,750

So, Money Makeover Inc. pays $36,750 in income taxes for the corporation. Now, let’s say you’re one of two shareholders for Money Makeover Inc., and you get a dividend of $25,000. Well, this is where things get a little complicated, so pay attention.

If you owned the stock longer than 60 days, it's called a "qualified dividend," and the IRS then will tax it on a sliding scale. That means the higher your dividend the more you'll pay in taxes. If your qualified dividend is lower than $38,601 (like in our example above), you wouldn't pay taxes. But the moment your dividend goes above $38,601, you start to pay the tax. The rate maxes at 20% for earnings over $425,800. Now, let's say you haven't owned the stock longer than 60 days. Then, it's called an "unqualified dividend." You’ll pay taxes on unqualified dividends by using your personal tax rate, which you’ll find in your tax bracket.

What’s the tax rate if you’re not a C-corp?

If your business is a sole proprietorship, partnership, LLC, or S corporation, calculating income taxes is much easier than C corporations. Whatever profit you make will be taxed once at your personal tax rate.

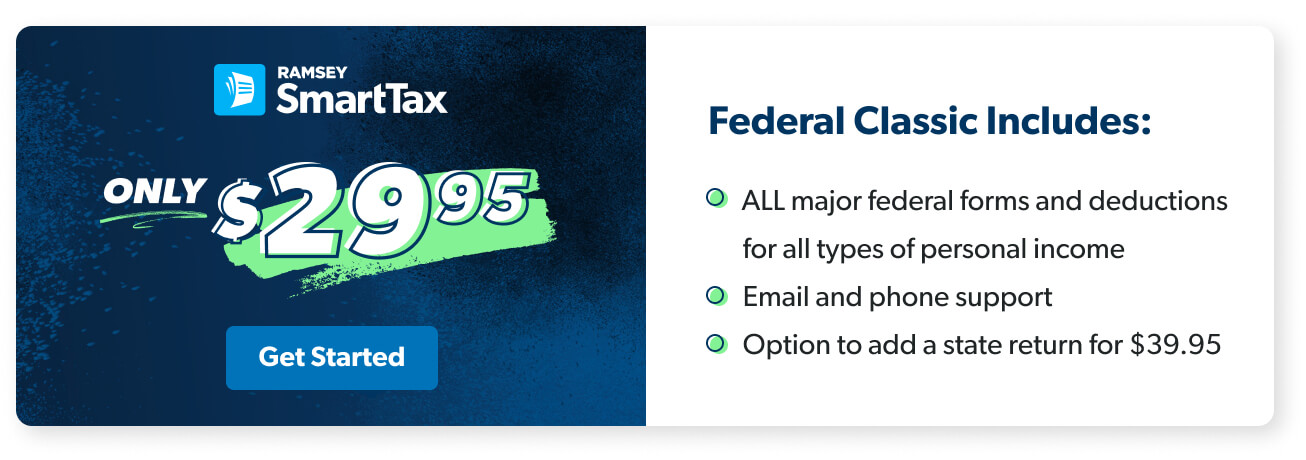

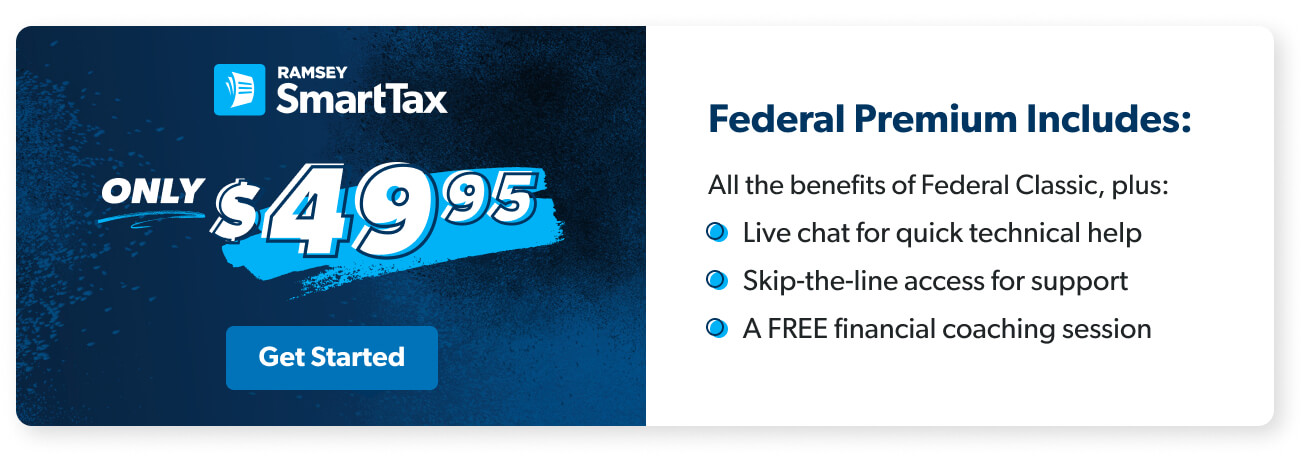

Got small business tax questions? RamseyTrusted tax pros are an extension of your business.

So again, let’s say you own a company called Money Makeover. Let’s also say your company makes $75,000 in profit. And let’s go ahead and say after business expenses, deductions and employment taxes (we’ll get to those next), you’re left with $50,000 in taxable income.

Now, if this is your only income and you’re not filing jointly with your spouse, then based on your tax bracket ($9,700 taxed at 10%, $29,775 taxed at 12%, and $10,525 taxed at 22%), you would pay $6,900 in taxes.

How Do You Calculate Employment Taxes for Small Businesses?

Hopefully you’re not tired yet, because we haven’t even touched on employment taxes. So far, calculating small-business taxes hasn’t been super difficult (if you’ve been on the struggle bus, you could use some tax help).

But when you start hiring people, you have to pay employment taxes, which breaks down into social security and Medicare taxes.

How do you calculate social security taxes?

All employees must pay social security taxes on income below $132,900 (if your income is above $132,900, you’ll pay taxes up to that amount).2 It’s super easy to calculate this tax. Just take 12.4% of your employee’s income and set aside 6.2% for taxes. Your employee will then pay the other 6.2%.

How do you calculate Medicare?

Everyone pays Medicare. To calculate this tax, take out 2.9% of your employee’s wages and set aside half, which is 1.45%.3 Again, your employee will pay the other half.

How Do You Calculate Estimated Taxes?

Now, here’s where things get tricky for small businesses. Unlike personal filers, who file their taxes once a year, small-business owners have to pay estimated taxes once every quarter. Yes, that’s four times a year.

Estimated taxes, or quarterly taxes, are based on what you expect your taxable income to be throughout the year. Yeah, that can be tough, especially if you’re just starting your small business. But once you’ve got an income estimate to work with, it’s really not so bad. Here’s a quick step-by-step process to help you figure out these quarterly headaches (sorry, taxes).

1. Estimate your taxable income this year.

2. Calculate how much you’ll owe in income and self-employment taxes.

3. Divide your estimated total tax into quarterly payments.

4. Send an estimated quarterly tax payment to the IRS.

Estimated taxes, or quarterly taxes, are based on what you expect your taxable income to be throughout the year.

How Do Tax Deductions and Credits Play Into This?

Tax deductions and tax credits are the biggest breaks you’ll get from the IRS. Deductions reduce your taxable income, while tax credits reduce the actual amount you owe to the IRS.

The biggest tax deduction for sole proprietors, partnerships, LLCs, and S corporations is a 20% deduction on all income.4 Yeah—20%. That means if your taxable income is $100,000, you can automatically deduct $20,000.

You can browse this list of common deductions to find out which ones apply to your small business, or talk to your tax pro.

The biggest tax deduction for sole proprietors, partnerships, LLCs, and S corporations is a 20% deduction on all income.4

Want to Never Do Small-Business Taxes Again?

Look, we get it. You have a company to run. If you’re sick and tired of balancing spreadsheets, filling out quarterly forms, and filing annual returns by yourself, take the next step and hire a tax pro. An experienced tax pro will not only save you time, but they can also save you money, since it’s their job to know more about taxes than you.

Don’t know where to find competent, trustworthy professionals? Don’t worry. We can help you find tax professionals near you—ones that Dave himself recommends.

Find a tax pro near you today.

Did you find this article helpful? Share it!

About the author

Ramsey Solutions